If you have ever put money into a traditional IRA or an old 401(k) at a former job, someone has probably mentioned a “Roth conversion” and your eyes may have glazed over. The idea is actually simple once you cut through the jargon. This article walks you through what a Roth conversion is, when it makes sense, when it doesn’t, and how to think about it for your own situation — in everyday language.

What Is a Roth Conversion?

There are two main types of retirement accounts most people run into:

- A traditional IRA or 401(k) is a pre-tax account. You got a tax break the year you put the money in, the money grows without being taxed along the way, but when you take it out in retirement, every dollar you withdraw is taxed as ordinary income.

- A Roth IRA is the opposite. You already paid tax on the money before it went in. From then on, the money grows tax-free, and when you withdraw it in retirement — contributions and growth — you owe nothing.

A Roth conversion is the act of moving money from the first kind of account to the second kind. The IRS treats the dollars you move as if you withdrew them, so you owe income tax on the amount converted in the year you do it. In return, those dollars never get taxed again.

In plain English: you choose to pay some tax today in exchange for never paying tax on that pot of money again.

The whole question is whether that’s a good trade for you.

The Decision in One Sentence

Convert if your tax rate today is lower than your tax rate will be later. Don’t if it’s higher.

That’s it. Everything else is just figuring out the two sides of that comparison.

Why Future Taxes Are Often Higher Than People Think

Most people assume “retirement equals lower taxes.” Sometimes that’s true, but often it isn’t. Here are the main reasons:

- Required withdrawals from retirement accounts. Once you reach age 73 (or 75, depending on when you were born), the IRS forces you to start pulling money out of your traditional IRAs and 401(k)s every year. These are called Required Minimum Distributions, or RMDs. They get larger every year, and for people who saved well, they can end up being bigger than their old paycheck was.

- Social Security on top. Once Social Security kicks in, it stacks onto your other income, and up to 85% of your benefit can be taxable.

- Losing a spouse. If one spouse passes away, the surviving spouse files taxes as a single person the following year — often on almost the same income. The problem is that single tax brackets are about half as wide as married brackets, so the same income can land in a much higher bracket.

- Medicare premiums. If your income is high enough in retirement, your monthly Medicare premiums go up — sometimes by hundreds of dollars per person. This is called IRMAA, “Income-Related Monthly Adjustment Amount, and it acts like a stealth tax.

Add it all up and a lot of retirees end up in the same tax bracket they were in while working, or even higher. That’s the surprise that makes Roth conversions interesting.

How Much to Convert: “Filling the Brackets”

Most people don’t convert their whole account in one shot. They convert a slice each year, sized to fit a specific tax bracket without spilling into the next one.

Quick reminder on how tax brackets work. Your income is taxed in layers. The first chunk is taxed at one rate, the next chunk at a higher rate, and so on. The rate on your next dollar is your marginal rate. The average rate across all of your income is your blended rate.

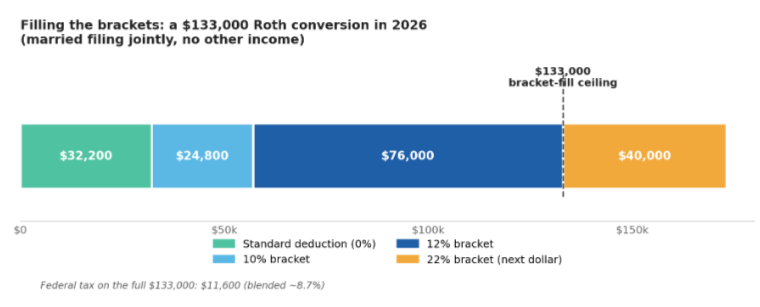

Here’s an example for a married couple in 2026 with no other income who converts $133,000 from their traditional IRA to a Roth:

- The first $32,200 is wiped out by the standard deduction. Tax: $0.

- The next $24,800 is taxed at 10%.

- The next $76,000 is taxed at 12%.

Total federal tax on the full $133,000 conversion: about $11,600 — a blended rate of roughly 9%. That is an extraordinarily cheap rate to lock in tax-free growth for the rest of your life.

Picture it as a stack of layers. Each colored block above is a tax layer. Green is free (the standard deduction), light blue is 10%, dark blue is 12%. Stack them up and you have filled the 12% bracket right to the brim — about $133,000 in total, taxed at a blended rate of less than 9%. The amber block on the right is the 22% layer waiting just past the dashed line. That is the cliff.

But here’s the cliff. The very next dollar above $133,000 jumps from 12% to 22% — almost double the rate of the dollar before it. That’s why people stop right at the top of the 12% bracket. It’s called “filling the bracket” — take advantage of the cheap layers, stop before the expensive one.

For single filers, the numbers are roughly half. The standard deduction is about $16,100, and you can convert roughly $66,500 before hitting the 22% layer.

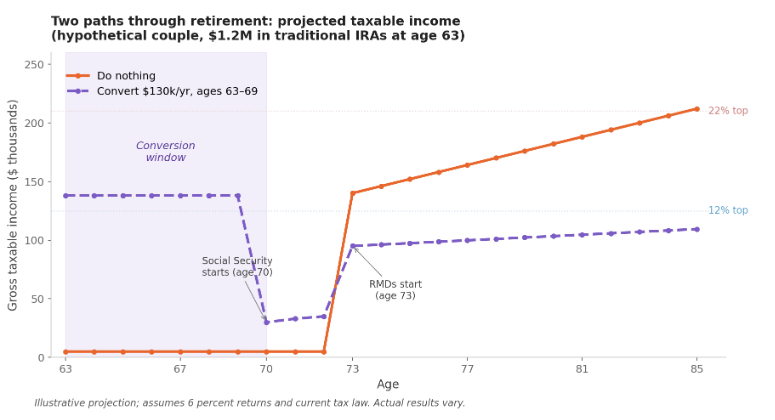

A Worked Example: Do Nothing vs. Convert

To make this concrete, imagine a married couple, both 63, with $1.2 million in traditional IRAs and another $300,000 in a regular taxable brokerage account. They just retired and plan to delay Social Security until age 70. Here are the two paths they could take:

Reading the chart: The solid orange line is the “do nothing” path. Their taxable income stays near zero through their 60s — looks great — then required withdrawals slam into them at age 73 and shove them into the 22% bracket for life. The dashed purple line is the “convert” path. They proactively pay tax in their 60s (the elevated line during the conversion window), but after age 73 their forced withdrawals are much smaller, and they spend the rest of retirement comfortably inside the 12% bracket.

Path 1: Do Nothing

From age 63 to 72, their taxable income looks great. Almost zero. Life seems good. Then age 73 hits, RMDs kick in, and — because the IRA has kept growing untouched — those forced withdrawals shove them into the 22% bracket. They stay in the 22% bracket for the rest of their lives. Every dollar of the IRA eventually comes out at 22%+ in tax.

Path 2: Convert Strategically

From 63 to 69, they run seven years of Roth conversions, each year filling the top of the 12% bracket — the same “fill the bracket” strategy described above. They pay tax now, at the low rate, but they’re shrinking the traditional IRA each year. At age 70 Social Security adds a small bump. By age 73, when RMDs start, the traditional IRA is much smaller, so the required withdrawals are much smaller. They spend the rest of retirement comfortably inside the 12% bracket.

The Trade

Yes, they paid more tax in their 60s than they would have under “do nothing.” But every year from 73 onward, they pay much less tax. Over a 30-year retirement, the difference typically adds up to six figures in lifetime tax savings. And whatever is left in the Roth account passes to their kids completely tax-free.

Is converting always better? No. If the market crashes right after converting, if one spouse dies young, or if tax laws change, the math shifts. But in most reasonable scenarios, the converting couple comes out far ahead.

When a Roth Conversion Makes Sense

- The years between retirement and Social Security. These are usually the lowest-income years of your life, and the best window for conversions.

- You have a large traditional IRA and many years before RMDs. Chipping away in your 60s softens the tax hit when forced withdrawals begin.

- You have outside cash to pay the tax. If you pay the conversion tax from the IRA money itself, you cancel out most of the benefit. The strategy works best when the tax is paid from a checking or brokerage account.

- You’re planning to move to a state with no income tax. Wait until after the move — you don’t want to pay your current state’s income tax on a big conversion.

- You want to leave money to your children. Heirs inherit a Roth IRA tax-free. They have to pay income tax on every dollar of an inherited traditional IRA, and current rules force them to empty it within 10 years.

When It Doesn’t Make Sense

- Your retirement income will be modest and stay in the 12% bracket anyway.

- You would have to use the IRA money itself to pay the conversion tax.

- You might need the money in the next 5 years (early withdrawal penalties may apply if you are under 59 and a half).

- You are on subsidized health insurance through the Affordable Care Act. A conversion raises your income for the year, which can wipe out subsidies worth $10,000 or more.

- You are on Medicare and near a premium threshold. Crossing certain income levels by even $1 can raise your Medicare premiums by more than $1,000 a year per person.

Important Details Before You Do It

- You cannot pick which IRA dollars to convert. All your traditional IRAs are treated as a single pool. If part of the pool came from non-deductible contributions, the IRS taxes you proportionally on the whole pool. This is called the pro-rata rule.

- There is no undo button. Conversions used to be reversible. They are not anymore. Once you convert, it is permanent.

- Your state taxes it too, if you live in a state with income tax.

- Each conversion has its own five-year clock. If you are under 59 and a half, you have to wait 5 years before tapping the converted money without a penalty.

How to Decide — Five Questions to Ask Yourself

- What is my tax rate this year, federal and state combined?

- What do I realistically expect my rate to be in retirement, once Social Security and RMDs are in the picture?

- Do I have cash outside the IRA to pay the conversion tax?

- Am I near any cliffs — ACA subsidies, Medicare premium thresholds, or the next tax bracket?

- Will I need this money in the next five years?

If your future tax rate looks meaningfully higher than today’s, you have outside cash to cover the bill, and you can stay below the cliffs, doing partial conversions each year is usually worth it — and it’s usually worth repeating every year until the math changes.

If any of those answers wobble, convert a smaller amount or skip the year entirely. There is no prize for converting on a schedule.

The Bottom Line

A Roth conversion is a tax-timing trade: pay now, save later. It works when “later” is a higher tax environment than “now.” For most people, the best window is the years between when work stops and when required withdrawals begin.

At IPS Strategic Capital, we provide a detailed analysis of when, where, how and why at no charge to all our clients. Please reach out today if you have any questions regarding if, when and how you should convert your retirement

General educational information, not tax, legal, or financial advice. Speak with a qualified professional about your specific situation.